We spend a lot of time discussing regulation in regards to Hive. Many of us maintain that, when it comes to the base layer, Hive cannot be regulated. Without the central point of entry, the vulnerability is removed. Even with that, some contest this idea.

For that reason, we will look at the most public regulator regarding cryptocurrency, the Securities and Exchange Commission (SEC). What would Gensler find if he looked at Hive?

This means we have to embark upon the Howey Test, the age old rule of thumb if an asset is a security or not. Looking into this means we can conclude whether Hive is like Ethereum, Cardano, and a host of other coins that are out there.

Please bear in mind, this is only going to apply to the base layer. We cannot say the same thing about layer 2 solutions.

Is Hive a security? Lets dig in.

Source

Investment Contract

When it comes to US Securities law, the idea of an "Investment Contract" is vital. This is what the Securities and Exchange Commision uses to determine if something qualifies or not. If it does, then it is the same as stocks and bonds.

This is from the SEC website regarding digital assets.

The U.S. Supreme Court's Howey case and subsequent case law have found that an "investment contract" exists when there is the investment of money in a common enterprise with a reasonable expectation of profits to be derived from the efforts of others.

It was further broken down into the following characteristics:

- an investment of money

- a common enterprise

- the expectation of profit

- derived from the efforts of others

Looking at these, we see the first three are met. So according to Howey, Hive is on pace to be a security.

It is the last one where it gets tripped up.

Active Participant (AP)

This is a term that is crucial to this aspect of the discussion.

Here we see how the SEC views it:

When a promoter, sponsor, or other third party (or affiliated group of third parties) (each, an "Active Participant" or "AP") provides essential managerial efforts that affect the success of the enterprise, and investors reasonably expect to derive profit from those efforts, then this prong of the test is met.

So the question is does an Active Participant exist on Hive? At the same time is this individual responsible for performing certain tasks that are necessary for one to realize the expectation of profit?

To get this answer, let us dive into the working of Hive.

Open To Anyone Running

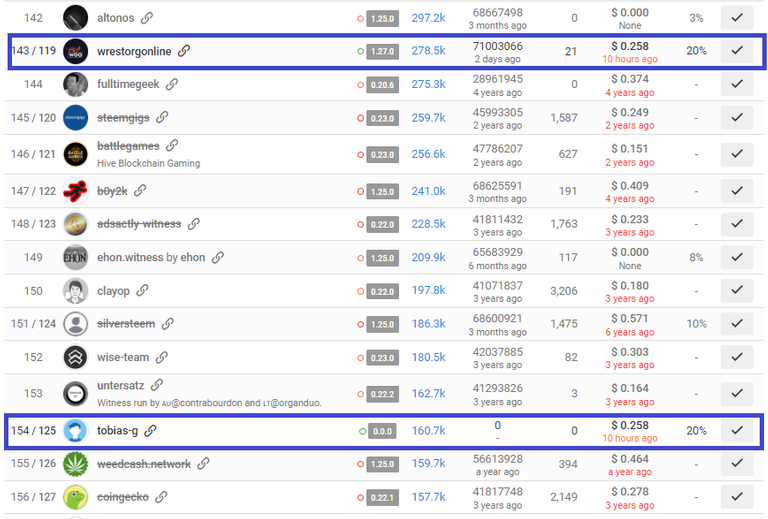

Hive operates on a Delegated Proof-of-Stake system that assigns block production on a rotation basis. That means anyone who sets up a node, running the software, will produce blocks. This is not up for debate or dispute. Anyone can produce blocks simply by setting up a node.

Here is a list of the lower ranked witnesses. Notice the one's highlighted (they are live) and how they produced blocks. One of the nodes was only recently set up.

The point here is the network is not dependent upon an Active Participant to keep things going. All nodes are run by unaffiliated users. The system is not dependent upon any project backer.

Hence, if any of the Top 20 witnesses closed down, regardless of who it is, the network would keep running. No single entity is essential for Hive to operate.

Software Development

The software is written. It is open source. Here again, anyone with the skills is able to update and add to it. Nobody can stop the community from participating.

Naturally, skill and ability factors into this. That said, those with the coding experience could produce the next version of the software.

Before getting to that, it is vital to understand the network is running. No software upgrades are necessary. Anything that is added is for enhancement, not necessarily for the operation of the network.

It might appear that there is only one set of software code. We often mention the "core developers". While this is not inaccurate, it can be a bit misleading. The reality is we have what is only one version of possible upgrades. Another group of developers could get together and write version 1.27.5 as it sees fit.

If that were to happen, then the block producers would decide which version to run. This would likely cause a great deal of conflict yet it is a possibility. What this means is we are not beholden to any one group or Active Participant for ongoing software development.

Anyone can step in and redo the code. The question ultimately comes down to will it be accepted by the community?

Access Coin

$HIVE is an access coin. This is the final piece offered up as evidence that it is not a security. The utility means that the purchase of the coin is not solely for speculation. In fact, that could be a secondary benefit.

The SEC points to the fact that courts have incorporated other considerations into the process. We will simply list them here:

- The distributed ledger network and digital asset are fully developed and operational.

- Holders of the digital asset are immediately able to use it for its intended functionality on the network, particularly where there are built-in incentives to encourage such use.

- The digital assets' creation and structure is designed and implemented to meet the needs of its users, rather than to feed speculation as to its value or development of its network. For example, the digital asset can only be used on the network and generally can be held or transferred only in amounts that correspond to a purchaser's expected use.

- Prospects for appreciation in the value of the digital asset are limited. For example, the design of the digital asset provides that its value will remain constant or even degrade over time, and, therefore, a reasonable purchaser would not be expected to hold the digital asset for extended periods as an investment.

- With respect to a digital asset referred to as a virtual currency, it can immediately be used to make payments in a wide variety of contexts, or acts as a substitute for real (or fiat) currency.

- With respect to a digital asset that represents rights to a good or service, it currently can be redeemed within a developed network or platform to acquire or otherwise use those goods or services.

- Any economic benefit that may be derived from appreciation in the value of the digital asset is incidental to obtaining the right to use it for its intended functionality.

- The digital asset is marketed in a manner that emphasizes the functionality of the digital asset, and not the potential for the increase in market value of the digital asset.

- Potential purchasers have the ability to use the network and use (or have used) the digital asset for its intended functionality.

- Restrictions on the transferability of the digital asset are consistent with the asset's use and not facilitating a speculative market.

- If the AP facilitates the creation of a secondary market, transfers of the digital asset may only be made by and among users of the platform.

Digital assets with these types of use or consumption characteristics are less likely to be investment contracts.

Going through the list we see these conditions met: 1, 2, 3, 5, 6, 7, 9

We can actually add to this by promoting the access coin aspect, thus fulfilling #8. There is also the fact that #11 is met although not facilitated by an AP (since there is none). The Internal Exchange is a secondary market that exists and can only be accessed by users of the platform.

To engage with the network, on requires Resource Credits which are derived from Hive Power. This is created by staking $HIVE.

Therefore, we have a use characteristic that makes the acquisition of $HIVE vital to different projects along with individuals.

Whatever happens to the market price of the coin does not impact one's ability to engage with the blockchain. This is determined be an internal set of metrics that have nothing to do with the market price.

Consumption Asset

This is a consumption asset. People wonder why $HIVE never takes off and the reason is simple: it is not purely for speculation.

We see there is a reason to hold it. As the network expands, we realize the price will likely follow. If the network grows in overall value, the ability to engage in it, thus, becomes more expensive. Here we see supply and demand take over based upon access and not speculation.

In summary, this fails the Howey Test and absolutely destroys the other considerations that courts use.

We are not dealing with a security in this instance.

This is not legal advice. It is an article written for informational purposes only. I am not an attorney and proper counsel should be sought out before indulging in any transaction of this nature.

If you found this article informative, please give an upvote and rehive.

gif by @doze

logo by @st8z

Posted Using LeoFinance Beta

{kind=link}